{kind=link}

This is not as big of an issue as you may think. The secret’s to mimic the “pay yourself first” approach by establishing an automatic contribution to your registered retirement savings plan (RRSP) that coincides along with your payday. A superb rule of thumb is 10% of your gross income. Remember that those staff blessed with an outlined profit pension contribute in regards to the same 10% rate (sometimes more) to their retirement plan normally. You have to follow these retirees step-by-step.

How much do you could have to save lots of in case you are 40 and don’t have any pension?

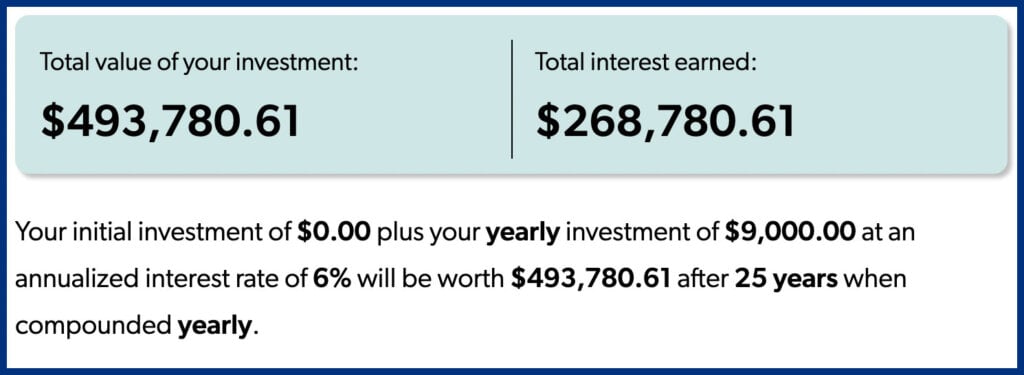

Let’s take a look at the instance of Johnny, who isn’t yet retired. He is a late starter who prioritized buying a house at age 35 and has not saved a penny for retirement by age 40. Now Johnny is wanting to start and invest 10% of his gross income of $90,000 per 12 months for retirement.

He does this for 25 years at an annual return of 6%, and by the point he turns 65, he has gathered nearly $500,000.

Remember, this does not take future salary increases under consideration. For example, if Johnny’s income increases by 3% annually and his savings rate stays at 10% of gross income, the dollar amount of his contributions would increase accordingly annually.

This minor change increases Johnny’s RRSP balance to only over $700,000 at age 65.

How government programs can assist people without pensions

A $700,000 RRSP – together with expected advantages from the Canada Pension Plan (CPP) and Old Age Security (OAS) – is enough to take care of the identical way of life in retirement that Johnny enjoyed during his working years.

Because once his mortgage is paid off, he’ll now not be saving for retirement and may assume that his tax rate in retirement can be significantly lower.

When Johnny starts taking his advantages at age 65, CPP and OAS will increase his annual income by nearly $25,000 (in today’s money). Both are guaranteed advantages which can be paid for all times and adjusted for inflation.