{kind=link}

The CAPE ratio evaluates a stock’s price in comparison with its average earnings over the past 10 years, adjusted for inflation. A high CAPE ratio suggests stocks could also be overvalued relative to historical earnings, indicating potential downside risks.

However, the image isn’t as clear because it seems. One of the most important disadvantages of equal weighting, as critics indicate, is the extra performance impact of the methodology.

Take the Invesco S&P 500 Equal Weight ETF (RSP) for example. Sales are 21% and the expense ratio is 0.20%. The Canadian-listed version is the Invesco S&P 500 Equal Weight Index ETF (EQL, EQL.F). In contrast, SPY has a revenue of just 2% and a lower expense ratio of 0.0945%.

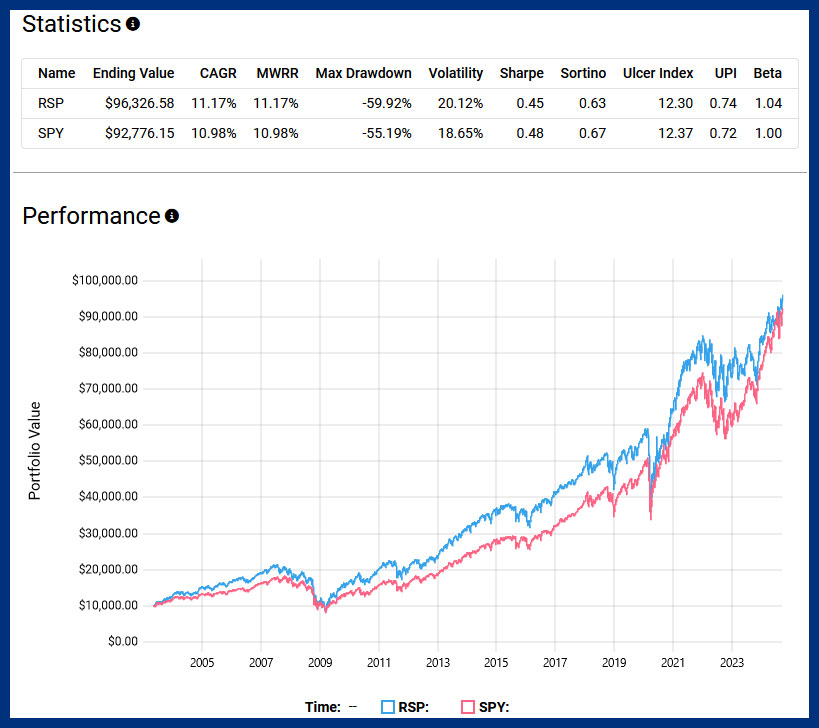

While it’s true that RSP has outperformed SPY in total returns since its launch in April 2003, the victory isn’t as clear-cut because it might sound. RSP’s risk-adjusted return, indicated by a Sharpe ratio of 0.45, is barely lower than that of SPY at 0.48. What does that mean? This could indicate that RSP accepted higher volatility to be able to achieve only barely higher returns. Additionally, RSP experienced a stronger maximum drawdown than SPY. A maximum drawdown measures the most important single decline from peak to trough during a given period and indicates the next historical risk of loss for investors.

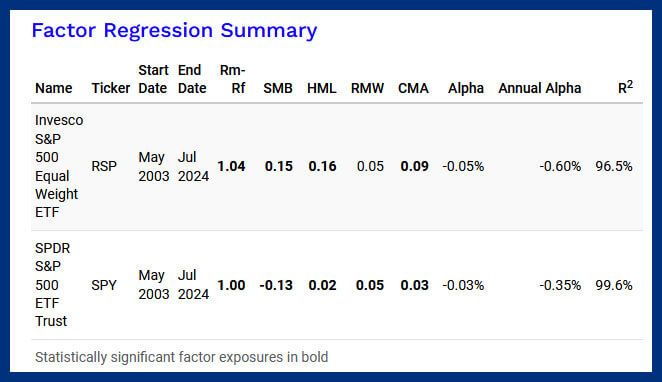

Further evaluation using factor regression shows that the majority of RSP’s outperformance comes from size. Essentially, RSP’s equal-weighted methodology inadvertently shifted exposure to smaller and more undervalued corporations which have contributed to outperformance previously.

This raises a critical point: If the goal is to take a position in a majority of these corporations, would not it’s easier and more efficient to focus on them directly based on fundamental metrics relatively than taking a blanket, equal-weighted approach to your entire S&P 500 track?

I’m now on the side of cap weighting. The most important appeal is its simplicity. Market capitalization strategies require fewer rebalancing or reconstituting decisions, which in turn keeps sources of friction resembling revenue and costs significantly lower – leading to fewer headwinds to performance.

In a really perfect, frictionless world, the appeal of equal weighting is obvious. However, the fact of quarterly rebalancing and better fees related to equal-weight ETFs has not historically resulted in higher risk-adjusted returns over the past twenty years.