{kind=link}

Java and Jgro look promising on the surface. Both ETFs bear the Morningstar medal force of “Silver”, a reputation that was given to funds that Morningstar analysts “exceed high conviction about the corresponding index or most colleagues via a market cycle on a risk-clear basis”. This isn’t a nasty confirmation when you trust the judgment behind it. (Gold values are for the highest 15%, with the silver rankings for the subsequent 35%.)

JPMorgan also promotes the relative historical outperformance of each funds. For example, Java emphasizes its results in comparison with the common of the Morningstar Large Value category and the Russell 1000 value index. JGro claims outperformance in the same way in comparison with her average of the Morningstar peer category.

US Active ETFs still have difficulty surpassing index

Benchmark comparisons could be rigorously chosen. Morningstar -analyst reviews are helpful, although they’re still subject to authority distortion. This means that individuals also put an excessive amount of trust in expert opinions, even when these experts could be biased or false.

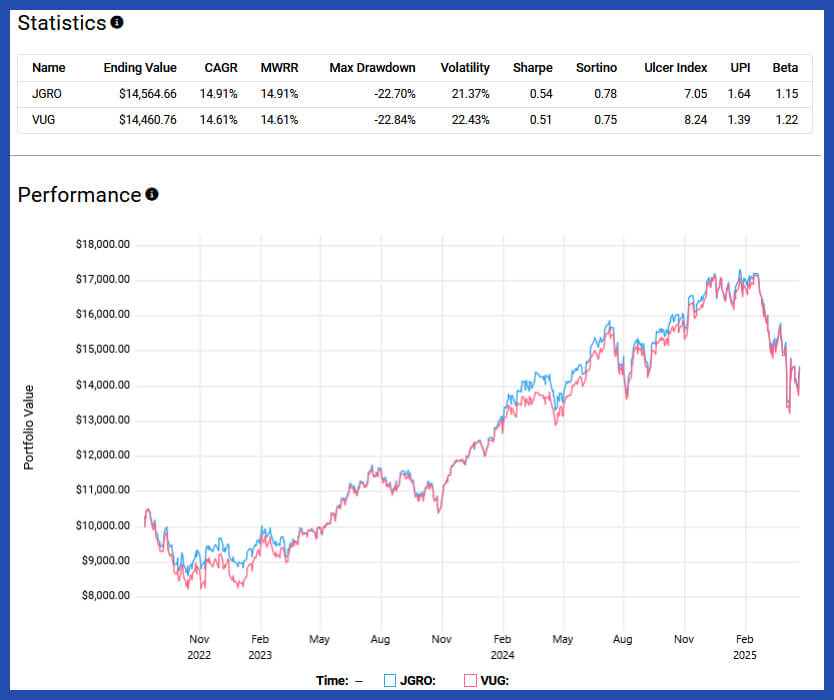

If you might be situated the historical returns directly with a large -available benchmark in comparison with far available benchmarks, you’ll draw a more mixed picture. From October 5, 2021 to

JGro, however, exceeded the Vanguard growth (VUG) only barely via his available window and returned from 14.61% of 14.91% CAGR from August 9, 2022 to April 23, 2025.

This raises the query: Why pay 0.44% for Java or JGro when VTV and VUG offer the same value and growth exposure with a big cap value with only 0.04%? The cost gap is considerable and it becomes even harder to justify yourself when you examine the portfolio overlap.

From April twenty fourth there was 99 overlapping stocks Between Java and VTV. This corresponds to 61.5% of the 165 stocks of Java and 30.4% of the 335 participations of VTV. This overlap indicates a meaningful degree of similarity between the 2 portfolios, at the least by way of core stocks.

For JGro, the overlap is a bit lower, but still remarkable. There are 58 participations with VUG, which is 51.8% of the 114 shares of JGro and 35.8% of the VUG-170. This also indicates that despite the energetic mandate between JGro and his index tracking counterpart, there’s a big common basis.