{kind=link}

From January to December 2022, the Vanguard Balanced ETF portfolio (VBAL), which accommodates a combination of 60/40, lost 15.04%, almost as much because the decline of 16.88%, which was recorded by the 100 percentpanguard-all equity Equity ETF portfolio (VEQT). The problem was not the stocks; Investors should expect volatility with them. It was the bonds.

When the rates of interest for combating inflation rose, VBAN’s binding component was hit hard. The above -average duration (a measure of interest sensitivity) led prices to diminish greater than short -term bond stocks. This aroused many conservative investors, especially those that believed that a set income would deliver ballast in a downturn.

In response to this, many portfolio strategists suggested a brand new model: the 40/30/30. That is 40% stocks, 30% bonds and 30% alternatives.

While institutions and consultants have access to stylish private alternatives to create this work, the query of whether Canadian retail investors can replicate the same structure with publicly listed ETFs. Here is my attitude and a few suggested ETFs to be exposed to the choice space.

What is the 40/30/30 portfolio?

The 40/30/30 portfolio is a conceptual framework that changes the normal balanced portfolio through bargains for alternative assets. The idea is to introduce a 3rd asset class that behaves otherwise than the opposite two.

Traditional diversification strategies failed in periods comparable to 2022, when each stocks and bonds have come together as a result of increasing inflation and rates of interest. The additional alternative sleeve is designed in such a way that in times when the opposite two pillars of a portfolio move in tandem, they protect the capital.

It will not be a uniform recipe. The 30%, which have been assigned to alternatives, can vary greatly depending on the preferences of the portfolio manager. In most institutional implementations conducted by consultants, this part could include:

- Hedge fund-like strategies Like boring equity, managed futures, long volatility and market-neutral approaches based on quantitative models and multi-asset exposure to attain absolute returns.

- Hard assets or digital value memory Such as gold, goods or cryptocurrencies comparable to Bitcoin, that are normally used as static assignments to compensate for traditional financial asset volatility.

- Private market investments comparable to private equity, private loans and direct real estate stocks that supply long-term return potential in exchange for liquidity risks and limited pricing.

The ETF Screener tool from Moneysense

Does the portfolio 40/30/30 work?

It is difficult to attract fixed conclusions, since two aspects limit the usefulness of most data which are used to support the 40/30/30 thesis.

The article is sustained under the promoting

X

The first is the survival. It is simple to look backwards and discover strategies that delivered a low correlation and solid returns, but that’s afterwards. Investors don’t necessarily have access to those means or a conviction in them if it was most significant. The danger is that the success stories of cherry nucers, which weren’t generally known or available at the moment.

Second, the outcomes are very dependent. The performance of a diversified strategy can vary sensibly depending on the beginning and end data. A number of good or bad years in alternatives can drastically distort the general return and the chance profile of a portfolio.

However, there’s a comparatively robust benchmark with over twenty years of knowledge that evaluated the liability of the concept: the MLM index. This benchmark pursues a scientific trend strategy in 11 raw materials, six currencies and five global bond futures markets. It weights each category based on historical volatility and the person contracts in the person weights in every basket. Although it doesn’t offer an ideal proxy for all alternatives, it offers rare long -term, transparent and rule -based data in a room that always lacks each.

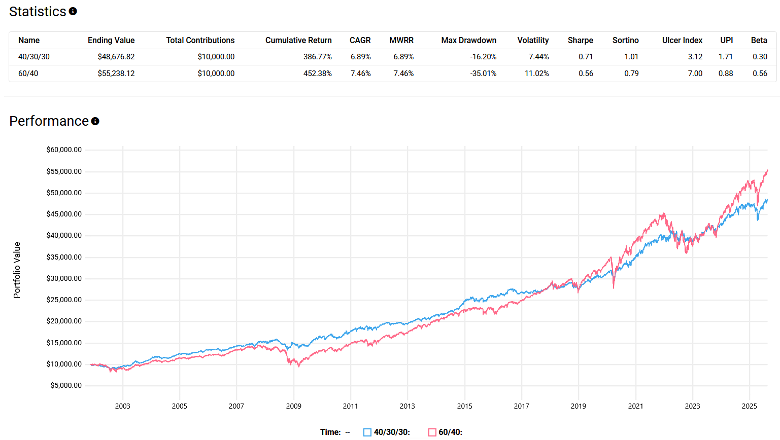

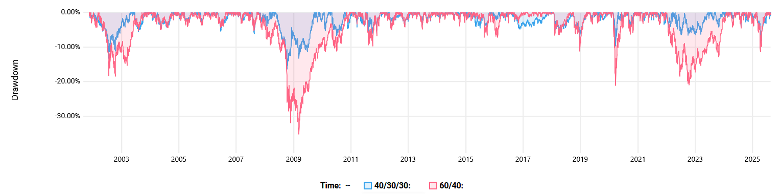

Use data from November 12, 2001 to August 19, 2025, a portfolio created with the S&P 500 with 40/30/30, Bloomberg US -AGGEGATE -DECHESINX and KFA -MLM index (balanced quarterly) below average a standard 60/40 mix with a complete interest of 6.89% of the compound annual growth rate (CAGR) against 7.46%. However, it was significantly exceeded on a risk-controlled basis, with a Sharpe ratio of 0.71 in comparison with 0.56.

It is much more essential that the diversification advantage was imposed than it was essential. The 40/30/30 portfolio showed higher down protection for essential stress events comparable to the bursting of the DOT COM bladder, the financial crisis of 2008, the crash of Covid-19 in 2020 and the bear market from 2022.

Investors can access the KFA MLM index via a US ETF: the crane-shares Mount Lucas Managed Futures Index Strategy ETF (KMLM). It follows the benchmark and is right with trend tracking of futures strategies in relation to raw materials, currencies and glued income.

The catch? Since KMLM is listed within the United States, Canadians are exposed to some hurdles: currency conversion, high administrative cost rate of 0.90% and a distribution tax of 15% by 15% distributions, unless they’re kept in a registered retirement savings plan (RRSP).