{kind=link}

A appears like an oxymoron, nevertheless it definitely exists. About 6% of U.S. households are millionaires, yet a lot of them still do not feel wealthy.

A is someone who’s value over $1 million but doesn’t have access to much of their wealth. In other words, your net value is extremely illiquid. A layoff, a bear market, or a job loss could quickly put them in danger.

In contrast, a person can also be value over $1 million but can easily access his wealth. They are liquid and resilient to financial shocks. Not only are you financially wealthy, but you’re also spiritually richer. The thought of monetary destruction rarely crosses their minds.

The most significant liquidity zapper for millionaires

The primary explanation for illiquidity is . Owning a phenomenal house is great, especially should you work at home or are retired. You just need to watch out about owning an excessive amount of home.

If you should stay comfortable, consider keeping your primary residence downstairs 30% of your net value. If you would like, keep it down 20%. This way, at the least 80% of your net value will be in liquid or semi-liquid assets.

In reality, maintaining 70-80% liquidity is difficult and unnecessary. Millionaires often put money into rental properties, private real estate funds, enterprise capital, enterprise capital, and other illiquid alternatives. Deca-millionaires and above also typically have significant private corporate capital, one other illiquid asset class.

That’s why at the least 20% of your net value in liquid assets– like stocks and bonds – is so beneficial. You’ll sleep higher knowing you will never need to sell illiquid holdings at bargain prices and can all the time have dry powder to purchase the dip when markets panic.

Recommended Income and Net Worth Chart Before Buying a House

Below is a handy home buying chart I put together based on income and minimum assets. Ideally, it is best to connect each really helpful income and really helpful net value to your goal home price. If not, you have to at the least one among the next mixtures before continuing:

- The really helpful income + the minimum net value OR

- The really helpful net value + the minimum income

Otherwise, you’re more likely to feel financially strained.

My experience with liquidity after greater than 26 years of constructing wealth

My recommendations are based on real-life experiences, from constructing wealth from nothing in 1999 to financial independence today.

With every home purchase since 2003, I’ve tracked how I felt about it. My final home purchase in 2023 was one other test of my 20-30% rule. It was an all-cash deal that represented about 23% of my net value.

The moment I closed, I felt uneasy—house wealthy and money poor—and hoped nothing bad would occur to our funds next 12 months. It was a terrible feeling that I desperately desired to do away with.

I even wrote about having to proceed living paycheck to paycheck after this purchase, which upset some people. But I just desired to be honest about how I felt. From this uncomfortable position, I made a decision to extend liquidity by negotiating more online deals and taking up a part-time consulting position at a seed-stage fintech startup. It’s a shame I only lasted 4 months because I didn’t benefit from the micromanagement.

The experience reinforced my belief: to feel truly wealthy and secure, Limit your primary residence to not more than 20% of your net value. Even though I survived the fear, I don’t need to feel that way again.

Thanks to a bull market and continued savings, my house now accounts for about 19% of my net value, and I feel great—almost like I got a free gift. What reinforced this sense was the sale of my old primary residence in early 2025 after renting it out for a 12 months. Converting this illiquid real estate capital into public stocks, treasuries and an open-ended enterprise fund that gives quarterly liquidity felt amazing.

As optimistic as I’m about single-family housing facing the west side of San Francisco, the safety that liquidity brings trumps every part.

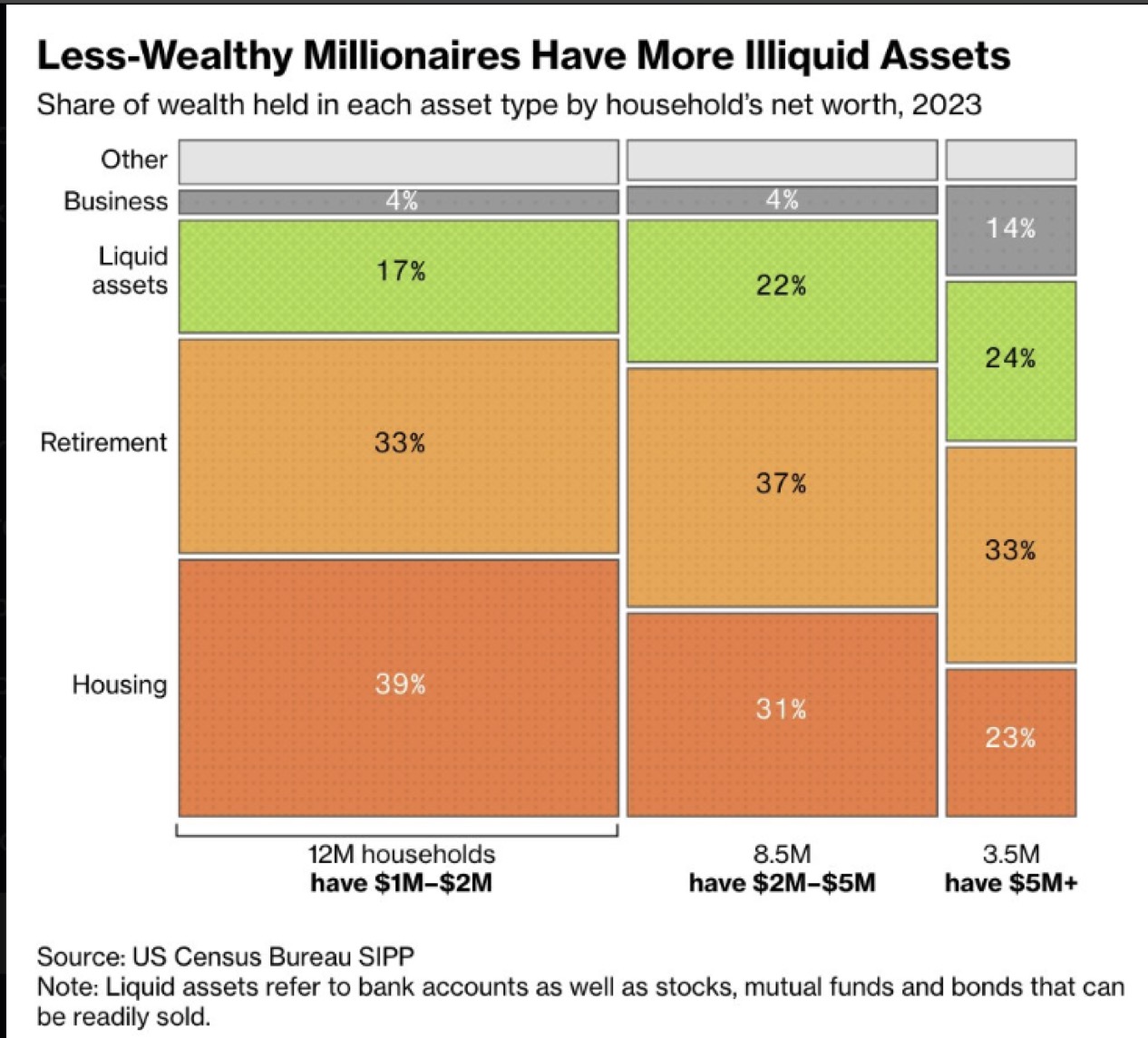

Liquidity by millionaire level

According to the newest data from the US Census Bureau, millionaires’ liquidity fluctuates widely.

For the ~12 million households with a net value of $1 million to $2 million, an aggressive 39% of the assets is tied up within the living space. It’s no wonder so a lot of these “poor millionaires” say they do not feel wealthy or feel like they’re stuck. Thanks to inflation, a millionaire today needs over $3 million to achieve the purchasing power of a Nineties millionaire.

In the meantime for the ~3.5 million households Only with a net value of greater than $5 million 23% is positioned in her primary residence. Approximately 33% comes from retirement accounts, 24% from money, 14% from business interests, and the rest from other assets. Much higher.

According to a survey by Financial Samurai, retirement net value is $5 million, closely followed by $10 million. Once you’re feeling wealthy enough, you are able to take motion, often by quitting a subpar job to pursue a more fulfilling endeavor.

I’m pleased that the 23 percent housing figure for these “rich millionaires” is consistent with my 20 percent guideline. I’m confident that for households value greater than $10 million, the housing share of net value would fall even further – probably below 20%.

I’ve already written about how you will feel whenever you reach various millionaire milestones – $1M, $5M, $10M and $20M+. And I can say with confidence that after you have got over $10 million and your house accounts for 20% of that, you’ll find a way to make it even in expensive cities like San Francisco or New York.

For example, for example you own a $2 million home with a mortgage, but have $4 million in a taxable brokerage account, $1 million in Treasury bonds, $2.5 million in an IRA, and $500,000 in money. I even have little doubt that you’ll feel wealthy.

This may sound obvious to you, but I can not let you know what number of expensive city dwellers have asked me what that magic number and ratio is so that they can finally get off the treadmill.

Housing creates basic wealth, every part else makes you richer

The Census Bureau data reinforces a crucial truth: Housing is the idea for constructing wealth.

Because of chronic undersupply, population growth, inflation, debt, forced savings, and government incentives, owning your individual primary residence is mostly a wise financial decision. You may not construct your wealth as quickly, but after a decade of home ownership, you’ll probably see significant capital gains.

The combination of paying off your mortgage and having fun with long-term appreciation is a strong force. Of course, there might be a greater time than others to purchase your primary residence. In the long run, nonetheless, you should get a neutral apartment in order that inflation doesn’t drive you into despair.

Temporary renting is wonderful, but not long-term (7+ years)

Some renters say they are going to “save and invest the difference,” but a minority actually do that consistently. Discipline over many years is tough. In a way, owning a house with a mortgage protects you from yourself and forces you to robotically save and construct wealth.

If everyone had perfect discipline, we’d all be in great financial shape with a 4 pack. Yet over 60% of Americans are obese despite being aware of the health risks.

I’m helping manage one among my relative’s investments without spending a dime. She is in her 50s and has lived in New York City for over 30 years. Unfortunately, she’s now under pressure to maneuver because her income hasn’t kept up with town’s relentless rent increases.

I feel the uncomfortable financial pressure from them and it really stinks. If only she had bought an apartment as an illustrator 10 or 20 years ago, her life could be much easier today.

The cycle repeats itself as soon because the share of residential properties reaches a small enough percentage

Once you own your primary residence and have achieved a “neutral” real estate exposure, you’ll be able to invest aggressively in other asset classes. Your foundation is laid. From there, other asset classes also can help expand your wealth. Over time, as these other investments grow, your primary residence will naturally represent a smaller percentage of your total net value.

Ironically, once your house falls under 10% of your net valueyou might feel. At this point, you are probably earning way over you’ll be able to spend on passive and lively income.

So do not be afraid to enhance your lifestyle. Buy a house value as much as 20% of your net value, and even one other 30% should you wish. Enjoy the fruits of your discipline after which reduce the ratio to feel one other great sense of accomplishment.

Housing forms your foundation, but liquidity creates your freedom. The wealthy millionaire not only has wealth, he can have it when it counts.

Invest in real estate without losing liquidity

If you’re thinking about investing in real estate without taking out a mortgage, it is best to have a look Call for donations. The platform manages over $3 billion in assets, with a give attention to residential and business properties within the Sunbelt.

With rates of interest step by step falling and recent construction limited since 2022, I expect upward pressure on rents in the approaching years, an environment that might be conducive to stronger passive income.

I personally have over $500,000 invested in Fundrise funds and so they are a long-time sponsor because our investment philosophies align.

If you should turn into a millionaire

Pick up a replica of my national USA TODAY bestseller. I even have over 30 years of monetary experience to assist you to construct more wealth and break free faster. Amazon is having a terrific sale at once.