{kind=link}

In an try to higher understand the potential discount or premium to NAV Fundrise Innovation FundI wanted to research Pershing Square Holdings, ticker symbol PSHZF, which is listed on the London Stock Exchange.

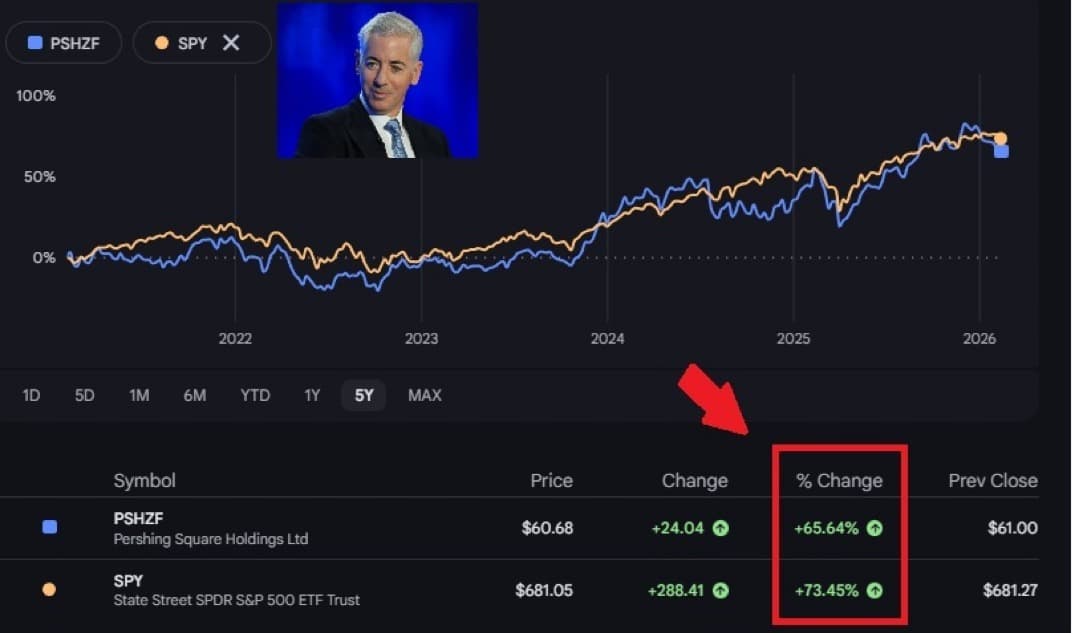

Pershing Square manages over $18 billion and is led by American Bill Ackman. Meanwhile, the fund is currently trading at a reduction of around 25% to its net asset value. When it was first listed in 2014, it traded at only a 9% discount. The NAV discount widened to around 40% in 2022 after which traded at a 30-35% discount in 2023 and 2024.

As an investor, you should use this historical discount-to-NAV range of -9% to 40% as an information point for when to speculate. Of course, the larger the discount to the web asset value, the higher the worth you get. If Ackman invests in winners, not only could the NAV rise, however the discount to NAV could also narrow.

If the Innovation Fund lists on the NYSE, could it trade at the same discount to net asset value as Pershing Square? It’s possible, but I highly doubt it for the explanations I highlight on this post.

Why is the Pershing Square Fund trading at such a big discount?

Here are 4 primary reasons for such a persistent discount to net asset value.

1) Core holdings are public shares

Pershing takes concentrated positions in 8-12 holdings and actively works with management to effect change. Previous investments include Chipotle, Restaurant Brands International, Hilton Worldwide, Alphabet, Canadian Pacific Kansas City and Amazon.

The problem with owning public stocks is that this . In other words, there isn’t any barrier to access to owning public stocks. Fund investors must depend on the acumen of Ackman and his analysts when determining when to purchase and sell.

Although many of the positions were public stocks, Ackman used credit protection to hedge downside risk through the COVID volatility in early 2020. So in the event you put money into a hedge fund and need protection against losses, Pershing can offer you that option. But normally that does not appear to be the case as they’re 90 to 100% long.

2) Closed structure + European listing

PSH is a London-listed closed-end fund and just isn’t a US-listed ETF.

This creates:

- No every day redemption mechanism to arbitrate price back to NAV

- A limited natural US investor base that doesn’t put money into LSE stocks or funds

- Less index inclusion in comparison with US funds

- Some institutional mandates that can’t own foreign-listed closed-end funds (CEFs).

If it were a US ETF with the very same portfolio, the discount probably would not be nearly as large. Maybe 0-5% as a substitute. Closed-end funds can trade at discounts for a long time if there isn’t any catalyst to shut the gap.

Unlike an ETF, there isn’t any easy mechanism that forces convergence, as I wrote in my post about trading various kinds of funds.

3) Fee structure (1.5% + 16% performance fee)

PSH fees:

- 1.5% administration fee

- 16% performance fee over a cap

This is cheaper than traditional 2/20 hedge funds, but expensive in comparison with passive equity exposure. Meanwhile, investors mentally discount future returns because fees increase.

When discounting expected future NAV growth through fees, some investors require a structural discount.

4) Concentration risk and volatility

Since the portfolio typically only includes 8-12 stocks, PSH has significant concentration risk that warrants a reduction. In good times the returns may be great. But in bad times, like in 2022, returns may be terrible, hence the 40% discount to NAV.

When investing in a hedge fund, your goal is often to cut back volatility and protect downside risk by hedging (shorting some names). However, if the Fund doesn’t hedge meaningfully or consistently and as a substitute creates additional volatility amongst holders who will not be qualified to achieve this, a reduction to the Net Asset Value will likely be required.

Given manager risk, key man risk and strategy cyclicality, a reduction to NAV is just natural.

Comparing Fundrise Innovation Fund to Pershing Square Holdings

Trading at a 25% discount to NAV after listing on the NYSE could be a terrible scenario for you Fundrise Innovation Fund (VCX) holders. However, I do not think this can occur due to following differences in comparison with Pershing Square Holdings:

1) VCX owns private, difficult to speculate assets

VCX owns coveted private company shares in names like OpenAI, Anthropic, Databricks, Anduril, SpaceX, Canva and more. Unlike public stocks, only a few people can invest directly in these corporations during their next private fundraising. Therefore, it’s logical that investors would pay an amount to own these names, not a reduction.

2) VCX trades on a much larger US exchange

VCX will seek to list on the NYSE moderately than the London Stock Exchange. In terms of total market capitalization, the NYSE is eight to nine times larger than the LSE. Trading volume on the NYSE is usually $50 billion to $100 billion per day, while on the LSE it is just $5 billion to $10 billion per day.

This means the natural demand pool is larger. VCX could be available to any U.S. retail brokerage account and will potentially attract institutional inflows.

3) VCX charges a much lower fee

VCX plans to charge a 2.5% annual management fee and 0% carried interest (a percentage of profits). PSH charges only a 1.5% management fee but, after a cap, 16% of profits, which is certainly one of the explanations Ackman is so wealthy. I’d much moderately pay 2.5-3% of AUM than 1.5% and 16% of profits for corporations which have the potential for huge growth.

If your position doubles from $100,000 to $200,000 in a single 12 months, you’d theoretically pay a fee of about $3,750 to VCX and keep $96,250 of the profit. In contrast, you’d pay a fee of $2,250 to PSH, plus 16% of the $100,000 profit, or $16,000, for a complete fee of $18,250. It is evident that paying a fee of $3,750 is preferable to paying a fee of $18,250.

4) VCX manages a smaller, more flexible fund with more holdings

VCX is a fund with a volume of roughly $550 million, PSH with over $18 billion. Therefore, it is usually tougher to outperform with such large assets under management.

For example, investing $55 million (10% of VCX) in a well-performing private growth company could make an even bigger difference for VCX than for PSH (0.3%). Acquiring the same 10 percent position, or a $1.8 billion PSH stake, would are likely to move the stock significantly and even make it unattainable if Ackman wanted to speculate in a smaller company given its limited float.

VCX owns at the very least twice as many corporations as PSH. However, about 75% of VCX is concentrated on OpenAI, Anthropic, Databricks, Anduril, dbt Labs, Vanta, Canva, and Ramp. Therefore, I’d say the concentration risk is comparable to PSH’s 8-12 corporations.

Conclusion on the PSH case study

I highly doubt the Innovation Fund trades at the same discount to Pershing Square Holdings. These are fundamentally different vehicles with different asset bases, fee structures, investor groups and structural dynamics. Although each are closed-end funds and lack the redemption mechanism of ETFs, the similarities largely end there.

Pershing’s discount is primarily a function of its public equity exposure, closed structure with no redemption mechanism, difficulty listing in Europe, performance fees and concentration risk. In contrast, VCX offers access to scarce private assets, intends to list within the United States, and has no burden of performance fees.

While no publicly traded vehicle is immune from trading at a reduction, directly applying Pershing Square’s historical discount range to the Innovation Fund is probably going the incorrect framing.

Destiny Tech100 (DXYZ) and Robinhood Venture Fund (RVI)

A more apt comparison could be DXYZ, which is currently trading at a premium of about 140% to its net asset value of about $11.50, and soon-to-be-listed RVI, the Robinhood Venture Fund.

Both own similarly hard-to-access private growth corporations which might be in high demand. It will likely be instructive to see whether RVI also trades at a premium to net asset value following its $1 billion offering. If that is the case, the probabilities of VCX trading at a premium increase and I’ll invest more in pre-listing VCX.

As we move closer to RVI’s listing, I plan to publish a follow-up evaluation examining how the corporate’s performance may impact expectations for the Innovation Fund.

I do that work mainly because I even have about $770,000 was invested within the innovation fundwhich could realistically fall by $150,000 or rise by as much as $385,000 based on listing dynamics alone.

Since my wife and I haven’t got day jobs, we rely heavily on our investments to fund our lifestyle. As a DIY investor, I want to conduct more thorough due diligence to enhance the probabilities of constructing informed, long-term investment decisions.