{kind=link}

However, this approach comes with trade-offs. Higher fees are an actual problem as many various strategies are based on energetic management. Complexity is one other. It’s tough to search out ETFs that really diversify returns and do not just repackage known risks. And even when the development is successful, a big gap stays. The portfolio is just not designed to guard against an actual market crash. When I speak about crashes, I mean sudden, deep, double-digit declines like through the 2008 financial crisis or the sudden collapse in March 2020 at the beginning of the COVID-19 pandemic.

Source: Testfolio.io

In the next sections, I’ll introduce two ETF approaches that retail investors have access to, highlighting Canadian-listed options when available. It’s value noting that the Canadian market is way more limited on this area than the US market, but you continue to have some options.

And while these strategies can provide protection in certain situations, there isn’t a such thing as a free lunch. As you will notice, the associated fee, complexity, and implementation challenges often make crash hedging ETFs difficult to make use of effectively, even for skilled investors.

Option 1: Inverse ETFs

Inverse ETFs are designed as short-term trading instruments that aim to attain the other return of a benchmark in a single trading day. Most track broad market indices, but some give attention to specific sectors and even individual stocks. The key point is that their goal resets every day. They usually are not designed to offer long-term protection.

This is a widely known US example ProShares Short S&P 500 ETF (NYSEArca:SH). On each trading day, SH seeks a return equal to the negative one-time of the S&P 500’s every day price return. If the index rises by 1%, SH should fall by about 1%. If the index falls by 1%, SH should rise by about 1%. In practice it does a superb job of providing this every day inverse exposure.

Leveraged inverse ETFs are also available for investors who want greater protection against losses. These use leverage to extend the inverse relationship. An example is Direxion Daily S&P 500 Bear 3X Shares (NYSEArca:SPXS)which goals for a negative every day return of 3 times the S&P 500. If the index falls 1% in a day, SPXS goals for a rise of around 3%. If the index rises by 1%, SPXS should fall by around 3%.

Canadian investors now have access to similar products. Instead of using US-listed ETFs, investors can search for options like this BetaPro -3x S&P 500 Daily Leveraged Bear Alternative ETF (TSX:SSPX).

The article continues below promoting

X

During sharp selloffs, these ETFs can do exactly what they were designed to do. During the COVID-related market panic in March 2020, when the S&P 500 crashed, inverse ETFs like SH and leveraged versions like SPXS surged, with leveraged funds seeing a significantly larger increase.

Source: Testfolio.io

As the chart above shows, the issue with these ETFs only becomes clear once the panic is over. As markets recovered after March 2020, each unleveraged and leveraged inverse ETFs began to say no steadily. This highlights the important thing limitation of those products: you can not buy and hold inverse ETFs in case you accept that stock markets are likely to rise over time. A sustained short position against the broader U.S. stock market is structurally a losing bet, which is why issuers are careful to notice that these products are intended for day trading only.

This creates one other challenge. Effective use of inverse ETFs requires anticipating the crash and positioning just before it occurs, then exiting before the recovery begins. This is market timing and it is not just an energetic strategy; it requires being right twice. Even skilled investors struggle with this on a regular basis, and retail investors are likely to fare worse.

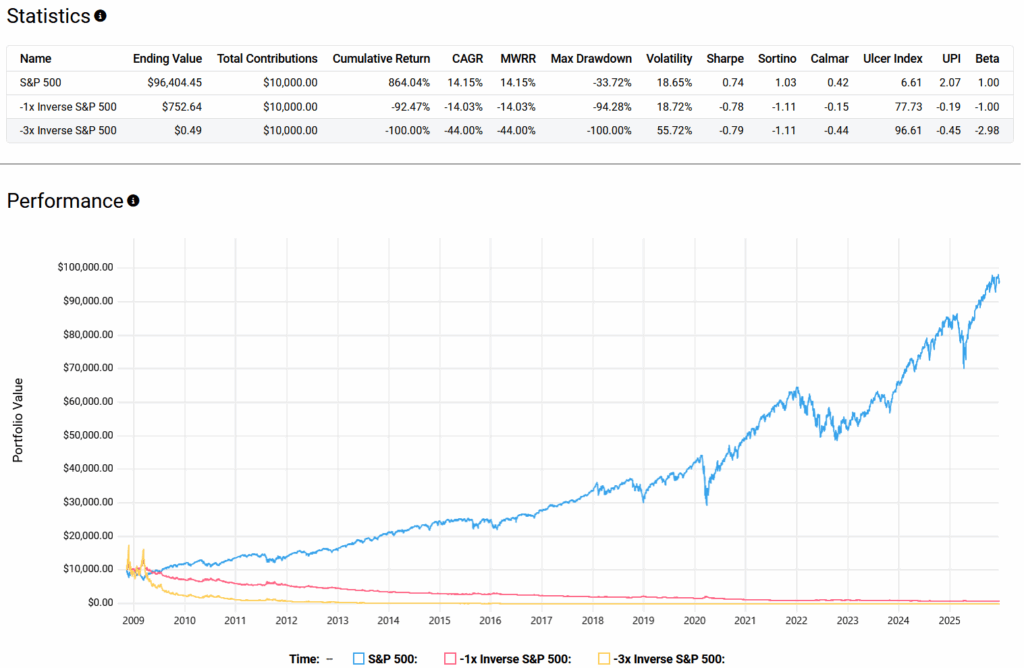

Long-term results reflect these headwinds. Over a period of roughly 17.1 years from November 5, 2008 to December 18, 2025, a buy-and-hold investment in inverse ETFs akin to SH and SPXS would have effectively fallen to zero after many reverse splits.

Source: Testfolio.io

This result is decided by several aspects. First, the underlying benchmark generally trends upward over long periods of time. Second, inverse ETFs have relatively high fees, with expense ratios of 0.89% for SH and 1.02% for SPXS. Third, every day compounding works against investors in volatile markets. As prices rise and fall, every day rebalancing causes losses to compound faster than gains, creating volatility resistance.

In short, inverse ETFs can provide short-term protection during sudden market declines, but their use as crash insurance requires precise timing. This makes them difficult to implement effectively and dangerous to take care of for greater than just a few days.