{kind=link}

Credit reports are more common than most individuals recognize – they usually can seriously affect their funds. A false entry could mean a rejected loan, higher insurance premiums or 1000’s more in interest over time.

You have the legal right to disclaim inaccurate or outdated information. You can correct these errors through measures and protect your credit.

This guide leads you thru the precise steps to search out mistakes, to submit a dispute and to pursue the credit stoves. So your credit is reflected in the reality.

What causes credit report?

Credit reports are surprisingly common – and in lots of cases they will not be brought on by something that they’ve done incorrect. These errors can come from the businesses that report their data or how one can match loan offices and display this information.

- Errors from lenders or data facilities – Banks, bank card firms and debt collectors sometimes report incorrect account details. A missing update or data input error could be displayed as a late payment or a false balance.

- Mixed or merged files – If someone has the same name or the same social security number, their information could be displayed of their report. This happens more often with common names or common addresses.

- Identity theft and fraudulent accounts – If someone uses their information to open credit accounts, these accounts can end of their report – even in the event that they haven’t authorized them.

- Reversed debts or double entries – Collections sometimes reset the date of an old fault in order that they’ve been searching for it these days, or a guilt can appear several times under different names.

Why are loan reporting errors

A single error in your credit will affect your creditworthiness and make borrowing costlier. Even a small error can cost it in the long term.

Errors can result in refused loan applications, higher rates of interest and fewer options if a loan, a mortgage, an apartment or a job are requested. In some cases, you possibly can increase your insurance premiums or trigger security deposits for supply firms.

Bad data in your credit won’t only be annoying – it is dear. With a mortgage of 250,000 US dollars, a lower credit value could increase your rate of interest and price you over 100,000 US dollars for the loan period. Fixing this error protects each your rating and your wallet.

Your rights under the law on Fair Credit Reporting Act (FCRA)

The federal law gives you the best to receive precise information in your credit reports. The Fair Credit Reporting Act (FCRA) is the law that protects it.

- You are entitled to a free report from every loan office every 12 months – Go to annual creditreport.com to request you.

- You can deny inaccurate or outdated information – If an article can’t be checked, the loan office must delete or correct it.

- Credit offices must investigate inside 30 to 45 days – As soon as you might have submitted a dispute, the office must reach the source of data.

- If changes are made, the office must notify others which have accessed their report – You can even ask you to send an updated copy to everyone who has drawn your report prior to now six months.

Ready to wash up your credit?

Find out how credit repair experts can support you in combating inaccuracies in your credit.

Step by step: How to make credit report errors

You don’t need a lawyer or a credit repair company to repair errors in your credit. Here you could find out how you possibly can do it yourself – step-by-step.

1. Check all three creditus for errors

First you get a free copy of your credit from each of the three large loan offices: Equifax, Experian and Transunion. Use annual creditreport.com, the one website approved by the federal law to offer you all three reports freed from charge.

Go through every report fastidiously. Find false account status, false credit, unknown accounts, double entries and outdated information. Also check your personal data resembling your name, your address and your employer.

2. Send a written dispute letter

You can deny online or by phone, but written letters are safer. They allow them to keep a paper lane and avoid given certain legal rights, which could also be distributed with in the event that they argue online.

Your letter should clearly discover every mistake, explain why it’s incorrect and contain all supportive documents that support your claim. List the account number and the loan office. You do not have to send a duplicate of your entire credit – just the page with the error.

You can use one in every of our free loan disputes to start. Just adjust it to your situation, print it and send it by e -mail with a requested return material.

3. Wait for the test results

After the loan office has received its dispute, you’ll start an investigation. You contact the lender or data provider to request a review. This company must check and report the account.

You normally get results inside 30 to 45 days. If the article is checked, it stays in your credit. If the corporate cannot check it or doesn’t answer in time, the loan office must remove it.

4. Follow -up, if you happen to don’t hear back

If 40 days have passed and you might have not received a solution, send a follow-up letter. Add a duplicate of your original dispute, each documentation you might have sent and proof that the office has received your letter.

If the loan office doesn’t respond or refuses to repair a transparent mistake, set a criticism with the one Consumer financial protection office Or the Federal Trade Commission. These symptoms can support your case if you happen to take further measures. Always hold copies of every part you send and receive.

Where do you send your in dispute

If you might be able to send your loan dispute, use the contact details for every following loan office. Always send your letters by e -mail and make a duplicate to your documents.

Equifax

Equifax Information Services LLC

Postfach 740256

Atlanta, GA 30374-0256

Telephone: (800) 685-1111

Expert

Expert

Postfach 4500

Allen, TX 75013

Telephone: (888) 397-3742

Transunion

Transunion LLC Consumer Dispute Center

Postfach 2000

Chester, PA 19016

Telephone: (800) 916-8800

What if the error is just not removed?

Sometimes the loan office doesn’t fix the error – even in case your documentation is evident. If that happens, you now not have options.

First send a second dispute with additional support documents. Be specific to what was previously submitted and why the article remains to be incorrect.

If you continue to don’t correct it, escalate. You can submit a criticism to the Consumer Financial Protection Bureau or the Federal Trade Commission. These symptoms don’t solve the issue overnight, but they create a paper lane that strengthens its case.

If a loan office or lender violates your rights as a part of the law on Fair Credit Reporting, you will have legal reasons to complain. Create detailed records within the event that you might have to talk to a lawyer for consumer protection.

When should help get help from a credit repair company

The dispute of credit fermentation errors requires time, patience and follow-up. If you might be overwhelmed or simply want another person to take care of it, a credit repair company might be considered.

The best credit repair services know how one can challenge inaccurate objects, pursue stubborn lenders and push in response to results. Look for firms with transparent prices, strong reviews and a hit story of success in disputes like yours.

Credit Saint is probably the greatest rated options. They have helped to remove 1000’s of individuals to remove collections, derivations, bankruptcies and other negative grades. If you might be ready for skilled support, start with free advice to see what is feasible.

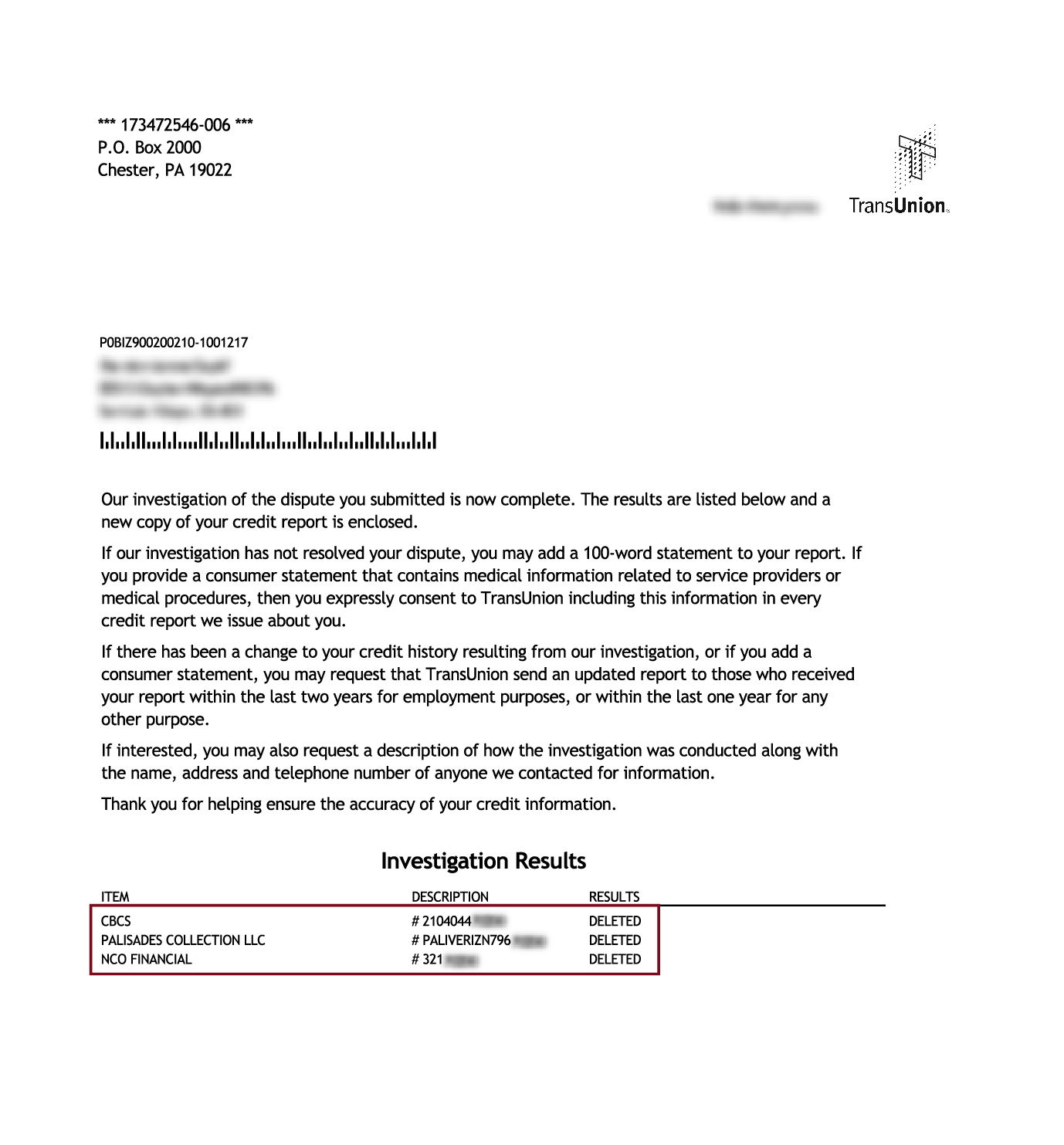

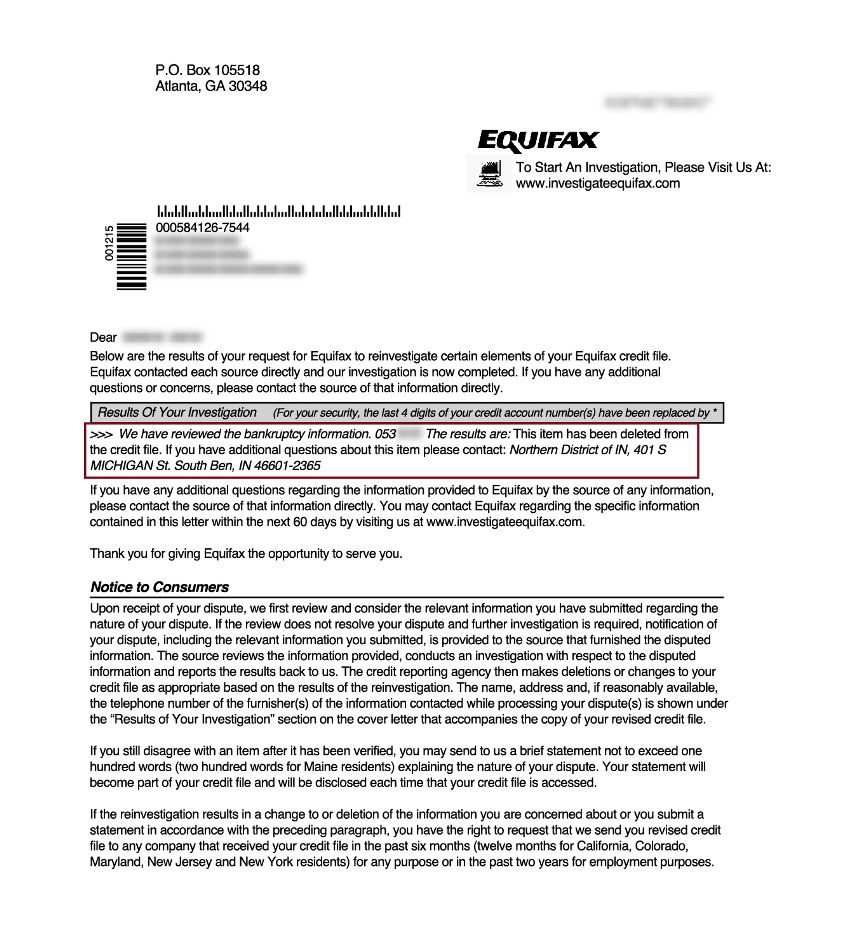

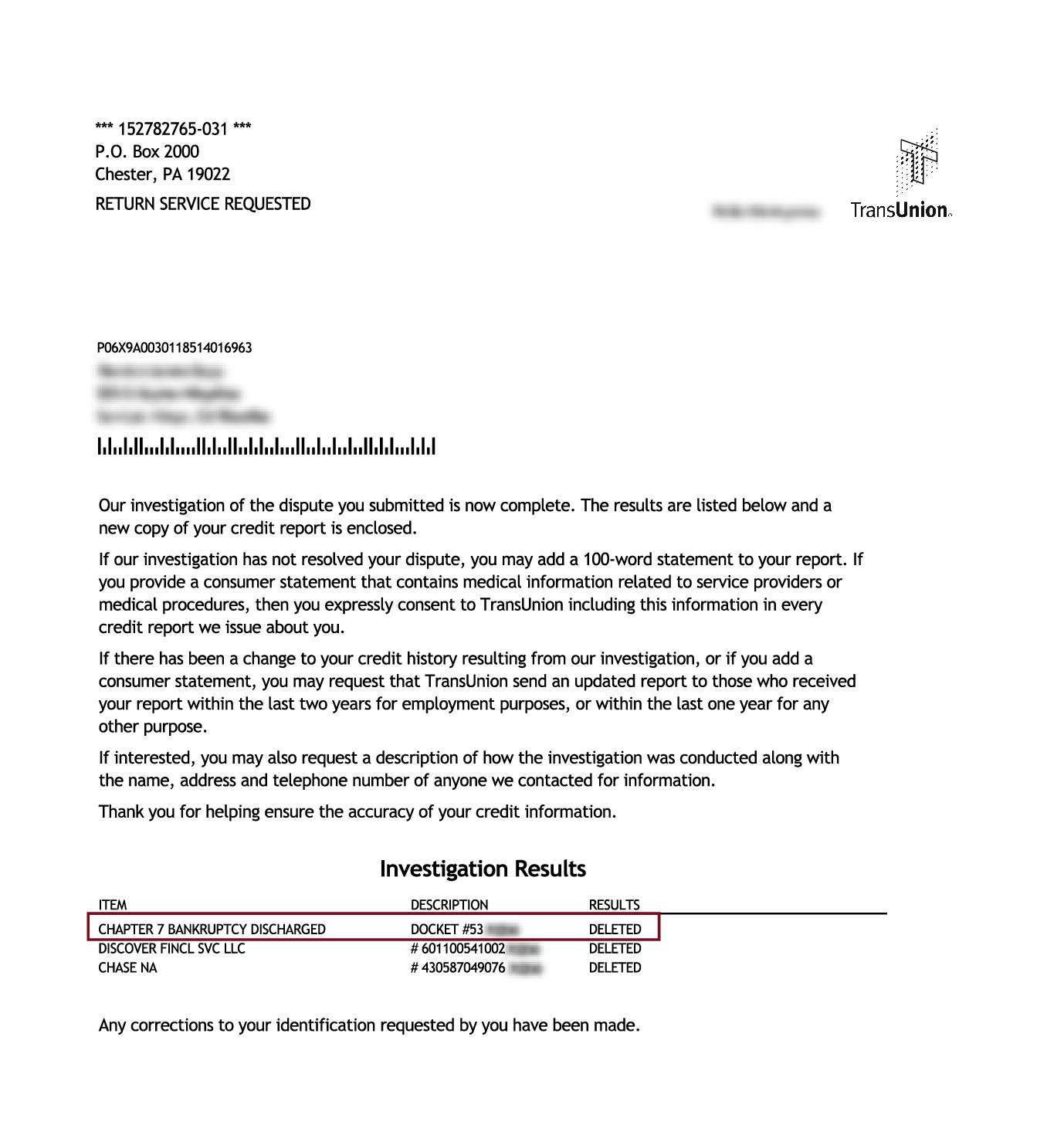

Real results from credit repair services

Are you wondering which credit repair can actually do? Here are real examples of negative objects which were successfully faraway from loan reports.

Click the photographs below to display them in full size.

Still today to repair your credit

You do not have to live with mistakes in your credit. Regardless of whether you take care of it yourself or hire an expert, crucial thing is to take measures.

Remove the inaccuracies, follow the creditworthiness and protect your creditworthiness. If you wish expert aid, you must consider free advice with Credit Saint to find out whether you fit well.

Ready to repair your credit?

Find out how one can get help with the assistance of errors in your credit, which could affect your creditworthiness.