{kind=link}

Afterwards there may be the Hamilton Canadian Bank Mean Reversion Index ETF (HCA), which follows the Solactive Canadian Bank Mean reversion Index TR. Every quarter, HCA distributes the three banks, which were recently below average, often 80% of its portfolio, and 20% the three who exceeded the banking (word game intends!) On the concept that underperformers could collapse.

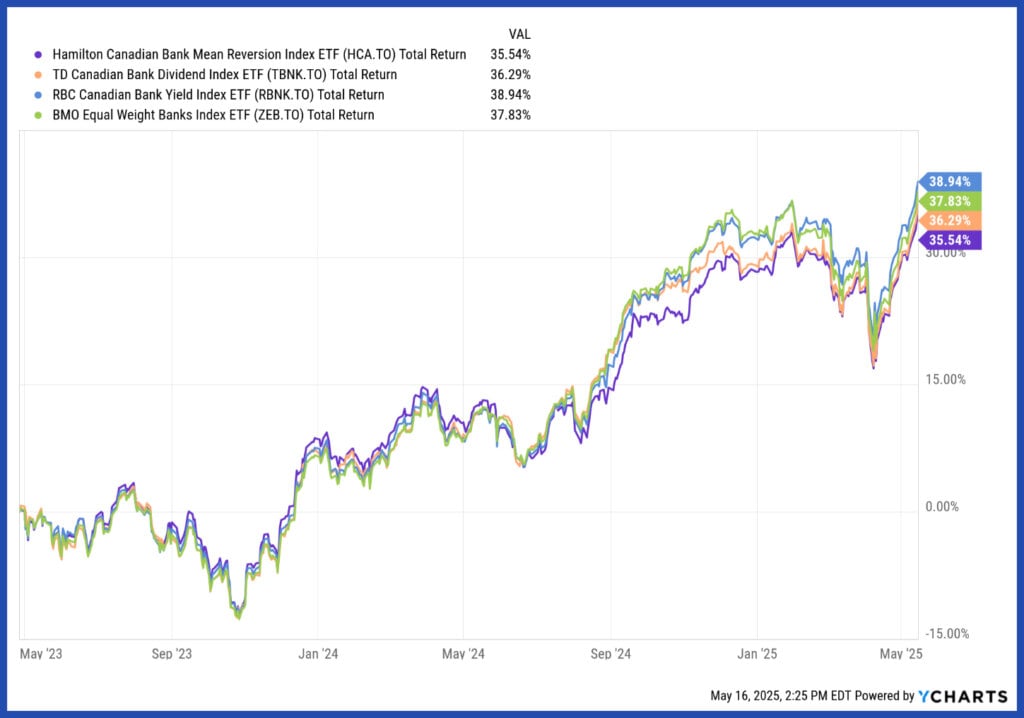

These custom strategies could be related to higher costs. TBNK calculates a 0.28%Mer, RBNK, at 0.32%, and HCA lists the list of 0.45%. So far, these additional fees haven’t transferred to great outperformance. From May 2023 to May 2025, the whole returns for these ETFs were cumulatively above or below the simpler equivalent zeb inside about 1%.

HCA, TBNK, RBNK and ZEB Historical Cumulative total returns

Application: These ETFs could also be suitable if you need to make your exposure a bit more fancier – a more energetic bet that exceed banks attributable to the dividend growth, return or the revenue – and conveniently pay higher fees for the chance (not a guarantee) of outperformance.

These ETFs fall under the roof of different strategies, which implies that they transcend traditional long-only purchases. They often use derivatives or leverage to enhance a side of exposure, no matter whether this can be a return, price returns or each.

A classic example is the BMO covered Call Canadian Banks ETF (ZWB). It holds all six large banks and reflects Zeb, but it surely lays a covers call strategy through the sale of options for its stocks. This limits on the pinnacle, but increases income and generates a return from dividend yields, capital gains and return on capital.

BMO sells these calls from money and at its own discretion, which implies that not every position is roofed in any respect times, which supplies the portfolio a bit more upward potential in comparison with systematic call -up strategies. You could get a solid distribution return of 6.66%, but with rather more muffled price growth.

The Hamilton Enhanced Canadian Bank ETF (HCAL) could be used for one more approach. No options are used in any respect. Instead, it turns the 1.25 -fold (125%) lever for the Solactive Equal Weight Canada Banks Index utilized by ZEB, Heb and HBNK.

In contrast to typical levers, that are reset each day via swaps, HCAL borrowed money using money loans, which implies that his returns will not be distorted by each day compounding. This setup increases each the upward trend and the drawback and likewise increases 6.42%, because the distributions are paid to the larger fictional exposure.