{kind=link}

As a toddler, did you ever dream of growing as much as be someone’s exit liquidity? Probably not.

But each time you purchase shares in an organization’s IPO, that is exactly what you develop into. Whether an early investor’s exit liquidity is nice or bad is difficult to say within the short term. In the long term you will certainly figure it out.

The essential reason I actually have invested a bigger percentage of my capital in private corporations over the past 20 years is because private corporations stay private longer. A bigger share of the profits goes to personal investors on the expense of future public investors.

SpaceX, for instance, was founded on March 14, 2002. 24 years later, on June 12, 2026, it would finally go public. Microsoft was private for 11 years, Google for six years, and Facebook for 8 years before going public. Those who bought their IPOs and held out did well. I’m unsure the identical thing will occur with SpaceX.

So probably the most common questions I get Newsletter readers Lately: Will you put money into SpaceX’s IPO?

My answer is NO for several reasons.

I don’t desire to have exit liquidity for big IPOs

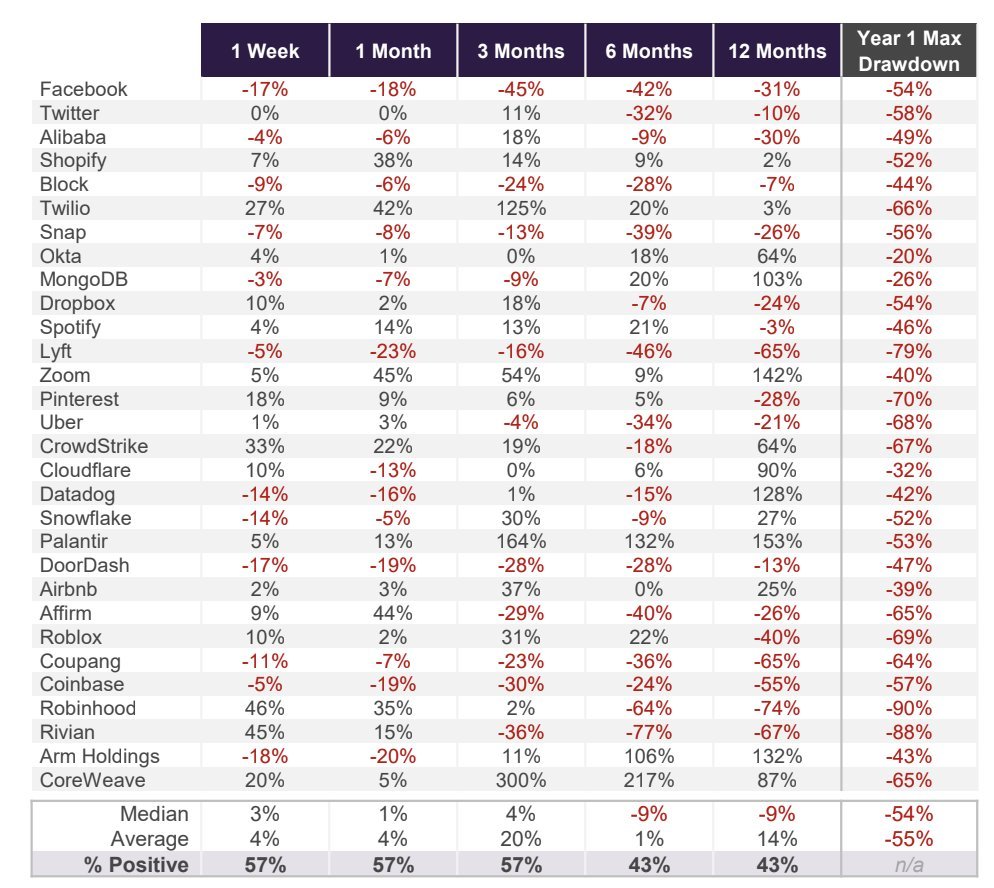

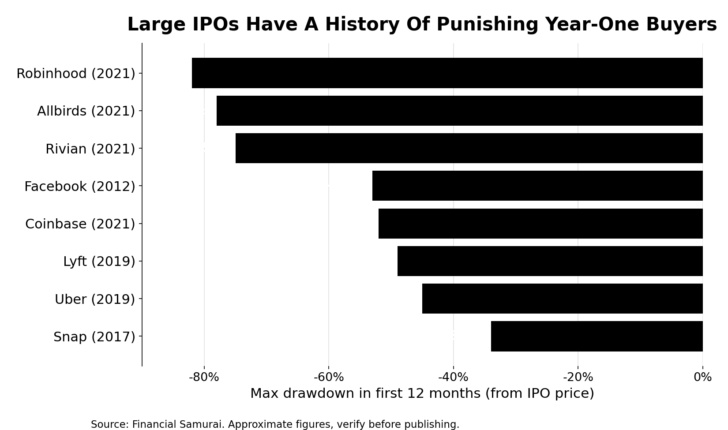

History is not kind to large IPOs ($1 billion+). Check out this chart showing the stock price performance of select major IPOs by post-listing period. Note the last column, “Maximum Drawdown for Year 1.”

The downside becomes even worse when you buy a big IPO that has a niche to the upside after which chase it. A newer example is Figma’s (FIG) IPO on July 31, 2025 at $33 per share. It gaped higher and peaked at around $122. Today the share price is around $22. That’s hard.

I don’t desire to be a part of the retail frenzy

Ultimately, Morgan Stanley valued Figma shares appropriately on the time. The retail frenzy was the essential reason the stock price shot up on the primary day.

I actually have been investing in public stocks since 1996 and have helped over 100 corporations go public during my time at Goldman Sachs and Credit Suisse. My experience is straightforward. Greater participation by retail investors results in more volatility, as retail investors are traditional paper traders and short-term investors.

So with SpaceX raising $75 billion, the most important IPO in history, and allocating 30% of the deal to retail, roughly $22.5 billion in shares, I see that as a net negative, not a net positive.

The volatility might be wild. If you take part in the IPO, you must closely monitor your position on the primary day and week. You might even take the day without work to develop into a manic day trader, which is one among the worst things you possibly can do in your returns.

I don’t desire to get out of liquidity because of outrageous valuations

At SpaceX’s (SPCX) goal price of $135 per share and the corporate’s value at around $1.77 trillion, the price-to-sales ratio might be greater than 90 to 1. I believe that is the very best P/E ratio in IPO history. Even IPOs that got here to market at half the value underperformed the market over the following three years.

Do you really need to remove liquidity from an organization trading at such an extreme valuation when the S&P 500 can also be at elevated levels and has much more mega IPOs behind it? I do not.

Here’s a glance back in any respect the businesses that made greater than 10 times their revenue on the dot-com peak and what happened next.

- Yahoo: ~50x sales. Rejected -97%. I didn’t wish to sell to Microsoft for $44 billion and ended up selling it to Verizon for a tenth of that.

- JDSU: ~50x sales. Rejected -99%. Parts dismantled.

- Qualcomm: ~30x revenue. Rejected -88%. It took about 20 years to interrupt even.

- Amazon: ~30x sales at peak. Rejected -97%. Obviously I’m an enormous winner now, but not without a whole lot of pain.

- Microsoft: ~25x sales. Rejected -65%. It took 16 years and eight months to succeed in a brand new high (October 2016).

- Cisco: ~25x sales, P/E over 200. Decline of -90%. In December 2025, 25 years and eight months later, the 2000 peak was finally broken.

- Intel: ~13x sales. Rejected -82%. In May 2026, almost exactly 26 years later, the 2000 peak was finally broken.

- Sun Microsystems: ~10x sales. Rejected -97%. Acquired by Oracle in 2009.

It is very important to speculate at reasonable valuations. Buying at a bargain price in an IPO is definitely the greater theory of folly, especially if the corporate will not be profitable. During the 1999 mania, I sat front row on the GS sales/trading floor at 1 New York Plaza. Many investors lost their shirts inside a yr.

The higher move is to attend for the hype to die down after which buy when you imagine in the corporate and its growth trajectory. Don’t let investing FOMO override your discipline. Retail has a incredible opportunity to supply hot IPOs to irresponsible levels, just for the value to correct as soon as management reports the primary few quarters.

Eventually you will own SpaceX anyway, so why chase it?

Here’s the kicker. With a valuation of $1.77 trillion, SpaceX debuts as one among the ten largest U.S. corporations. Index funds might be forced to purchase it sooner or later, which suggests you will even be forced to routinely buy it through your S&P 500, NASDAQ, and overall market funds.

You do not have to follow the IPO to own SpaceX. Wait just a few quarters and the market will hand you a position on the actual selling price. Let the index do the work.

And remember, most retail investors aren’t going to get IPO shares for $135 anyway. They receive a small allocation, if any.

For almost everyone, “buying the SpaceX IPO” really means buying SPCX on the primary morning after it has already gapped up (or down). This will not be a purchase order for the IPO. This is the voluntary provision of exit liquidity.

Already owns shares in SpaceX through enterprise capital

Finally, I don’t desire to lose SpaceX’s exit liquidity since I already own funds which might be more likely to sell some or all of their SpaceX shares on the IPO or after the lock-up period expires.

A conventional enterprise capital growth fund that I invested in in 2022 had about 10% of its fund in SpaceX in the primary quarter of 2026. I expect they are going to sell the complete stake sooner or later since they’re obligated to return capital to the LPs.

I also own a good portion of Fundrise Innovation Fund, VCX, which held an roughly 5% stake in SpaceX as of Q1 2026. VCX will not be required to sell anything that goes public because it is a everlasting capital fund.

All in all, I hold a big enough position in SpaceX that it could not be advisable to purchase more from a risk-return and asset allocation perspective. And even when I didn’t own any of it through enterprise funds, I still would not buy the IPO for the explanations mentioned above.

What I’d actually do as a substitute

To be fair, that is about buying millionaires and making them wealthy as a substitute of poor. Starlink is now an actual money flow machine, Starship could open up an entire recent market and there isn’t any comparable competitor. If you’re thinking that SpaceX is becoming the AWS of space, $135 might sound low-cost in ten years.

I’m not saying SpaceX is a nasty company. I say that I don’t desire to pay any price for an incredible company. The price protects you if the story falters.

So what would I do? I’d wait. Let the lock-up period expire, let the primary earnings reports are available in, let the frenzy burn off. If business is pretty much as good because the bulls say, it would be just pretty much as good at $110 because it was at $135. And if not, I’m glad another person figures it out first.

If you simply should own stocks, then buy them with disposable money that you would be able to 100% afford to lose.

But as a long-time Tesla shareholder, I actually hope SpaceX buys Tesla at a 50% premium.

Reader questions and suggestions

.