{kind=link}

CRE investors (CRE) for business real estate (CRE) have undergone brutal downturn since 2022. The mortgage rates of interest increased than inflation was higher, expanded the capsins and fell the assets across the board. The rally scream was easy:

Now that we’re within the back half of 2025, the worst appears to be over. The business real estate recession appears to be over and the prospect knocks again.

I’m confident that the following three years might be higher in Cre than the last. And when I’m incorrect, I just lose money or earn lower than expected. This is the worth we as investors pay in risk assets.

A couple of years for business real estate

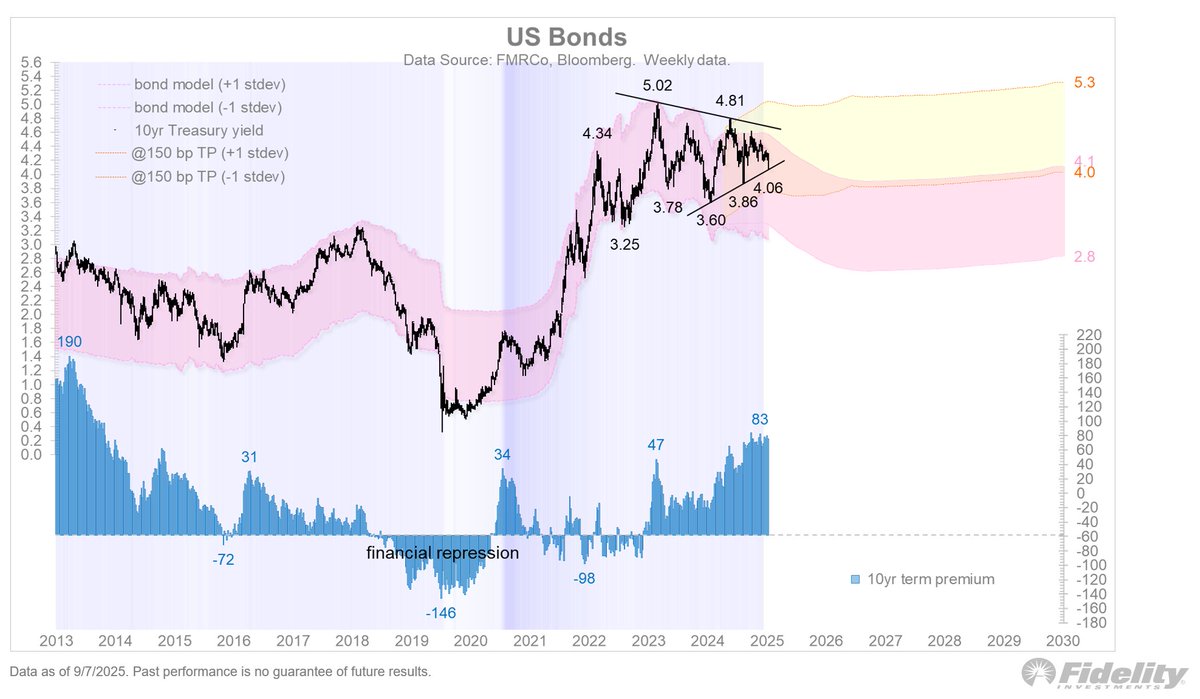

In 2022, when the FED had began its most aggressive cycle in installment growth for many years, Cre was considered one of the primary victims. Real estate values are incredibly sensitive to credit costs because most shops are financed. Since the 10-year-old state yield of ~ 1.5% pre-pandemic (low from 0.6%) rose to ~ 5% at the height value of 2023, the cap rates didn’t proceed anywhere.

In the meantime, the demand for office space, which were turned together as hybrids and distant work. Apartment developers were confronted with increasing construction costs and slower rental growth. Industrially, once the darling of CRE, frozen the availability chains after which normalized.

With the rise in financing and the NOI growth, the CRE investors needed to reflect. Headlines for default settings, extensions and “expansion and pretended” loans dominated the room.

Signs the business real estate recession ends

Fast result in this present day, and the landscape looks very different. Here is the rationale why I believe we’re at the tip of the CRE departure:

1. Inflation has normalized

Inflation cooled down from lower than 3% from a scay in mid -2022 in mid -2022. A lower inflation gives the FED coverage to facilitate politics, and investors are more confident within the junction of long-term deals. Price stability is oxygen for business properties and at last back.

2. The 10-year return is

The 10-year-old Ministry of Finance, which promotes most mortgage interest, has now dropped from ~ 5% to ~ 4%. This decline of 100 BPS is vital for levered investors. Lower loan costs by 1% can bypass the mathematics CAP rate in 10%+ higher property values.

If the 10-year-old return on government bonds can reach 3.5% and the common 30-year-old fixed rate of interest to five.5%, I expect an awesome increase in real estate demand. We are usually not that distant, especially if the FED cuts 100 basis points (1%) next yr.

3. The Fed swiveled

After greater than nine months of equality, the Fed cuts again. While the Fed does indirectly control the long -term mortgage interests, the cuts are filtering through on the short end basically. Psychological shift can be necessary: investors now imagine that the stripping cycle is basically behind us.

The following diagram shows about six FED installments by the tip of 2026, which is an overall display of ~ 1.5%. Such market expectations will change over time, but we’re here.

4. Increased tremendous peak

We have already seen the forced sellers, the credit extensions and the markdowns. Many of the weak hands were rinsed out. The sale of Not Schweigs, once an indication of pain, begins to draw opportunistic capital. Historically, this transition marks the rationale for an actual estate cycle.

5. Capital returns

The capital comes back after two years on the side. Institutional investors are underweight real estate in comparison with their long -term goals. Family offices, private equity and platforms resembling Firm Collect and put a refund into CR. Liquidity creates price stability.

Where the chances are high in CR

Not all CRes are the identical. While the office has been impaired for years, other real estate types are mandatory:

- Membership house: Rental growth slowed down, but didn’t collapse. Since there was only a brand new constructing on recent constructing products since 2022, undersupply and upward rental pressure will probably occur in the following three years.

- Industrial: Storage and logistics remain long -term winners, even when the expansion has cooled from pandemic.

- Retail: The “retail apocalypse” was overvalued. The well -founded centers anchored with food appear and the experience trade has the strength.

- Specialty: Data centers, senior residents’ apartments and medical office proceed to draw area of interest capital. With the AI boom, data centers are prone to see the biggest CRE investment capital.

As a capital allocator, I’m interested in relative value. Today, shares act at ~ 23x forward result, while many CRE assets are still everlasting than the tariffs at 2023 levels. This is a separation that’s price listening to attention.

Do not confuse business properties with your property

An necessary distinction: business properties are usually not the identical as their essential residence. CRE investors are hyper-oriented on yields, capsins and financing. Home buyers, then again, focus more on lifestyle and advantages. As a result, the rise in rates of interest tends to have less negative effects on dormitories.

For example, I purchased a brand new home in 2023 in order not to maximise the financial returns, but because I wanted more land and a closed outdoor area for my children while they’re still young. The ROI about soul peace and childhood memories are immeasurable.

In contrast, business properties are numbers. It’s about money flow, lever and exit people. Yes, emotions sneak up, however the market is way more ruthless.

Risks remain in CR

Let us be clear: If you call the tip of a recession, this doesn’t mean blue sky perpetually. Risks remain:

- Office clamp: Many CBD office towers are functionally outdated and might never get well.

- Debt cases: In 2026–2027 there remains to be a wall with loans that might test the market again.

- Political risk: Tax changes, zoning laws or one other unexpected inflation flare can derail progress.

- Global uncertainty: Geopolitical tensions and slowing down abroad could flow into the CRE demand.

But the cycles don’t end with all of the risks which have disappeared. They end when the balance between risks and rewards is shifting in favor of investors who’re able to look ahead.

Why am I optimistic about CRE

About 40% of my net assets are in real estate, with ~ 10% of them in business real estate. So I felt this down person.

But when I’m going out, I see Echo’s past cycles:

- Panic sales, followed by Opportunity purchase.

- Interest rates at the highest value and start to sink.

- Institutions that move back to the crime from the defense.

I recently recorded a podcast with Ben Miller, the CEO of Firmwho might be optimistic about CR in the following three years. His perspective, combined with the improved macro background, gives me the trust that we’re turned across the corner.

CRE: To thrive by survival

The mantra has been doing well for 3 years, we’re doing here. CRE investors who stopped at May are finally rewarded. Inflation drops, the interest loosens, the capital flows back and recent opportunities arise.

The end of the business real estate recession doesn’t mean easy money or a right back rash. In contrast to stocks that move like a speedboat, real estate moves more like a brilliant tanker – it takes time to show. Patience stays essential. Nevertheless, the flood has shifted, and that is the moment to re -position portfolios, acquire attractive reviews and prepare for the following upcycle.

The secret’s to stay selective, to maintain a protracted -term attitude and to align every investment together with your goals. For me, business real estate stays a smaller, but still significant a part of a diversified assets.

If you’ve gotten waited to the sidelines, it might be time to get in again. Because when investing, the perfect opportunities rarely appear when the water is calm – they show themselves when the cycle turns quietly.

Invest diversified in CR

If you would like to take care of business properties, take a take a look at Firm. Fundrise was founded in 2012 and now manages over 380,000 US dollars over 380,000 investors. Her focus is on private oriented business properties in lower market markets. Fundrise continued to take a position capital throughout the downturn with a view to record opportunities for lower rankings. Now how the CRE cycle turns, they’re well positioned to learn from the rebound.

The minimum investment is simply $ 10, which is simple for the common of dollars over time. I personally invested six figures within the CRE offer from Fundrise, and I appreciate that your long-term approach matches my very own. Fundrise was also a protracted -time sponsor of Financial Samurai who speaks for our joint investment philosophy.